“Managing liquidity in a volatile and uncertain business environment“

Introduction to Liquidity Management

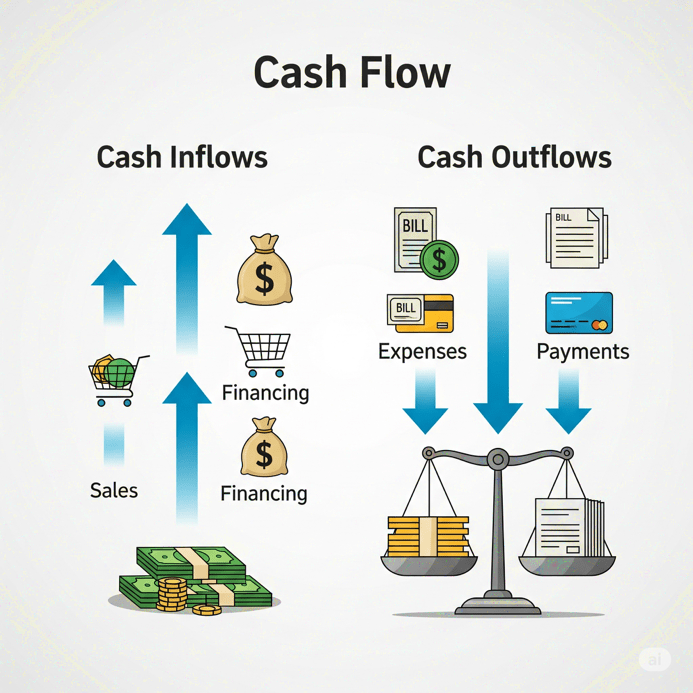

Liquidity refers to the availability of cash or easily convertible assets that businesses use to meet their financial obligations. Companies rely on the cash they generate—either through profits or financing—to carry out day-to-day operations, such as paying rent, salaries, purchasing raw materials, and acquiring services.

When businesses sell their products or services, they receive cash inflows. However, they also need to make payments for various expenses. A liquidity crunch arises when cash outflows exceed inflows—for example, when a company needs to make payments totaling ₹100 but only has an income of ₹50. In such situations, maintaining operations becomes challenging,threatening business continuity.

This challenge is exacerbated in a volatile and uncertain business environment, where factors like fluctuating sales, rising input costs, inflation, and unpredictable investment returns impact a company’s financial stability. For instance, during inflationary periods, raw material prices may rise, squeezing profit margins. Similarly, uncertainty about returns can discourage investments, or worse, lead to losses.

This article explores how businesses can effectively manage liquidity amid such volatility and uncertainty, ensuring financial resilience and sustainability.

Understanding Liquidity Challenges in Volatile Markets

In volatile business environments, managing liquidity becomes particularly challenging. Revenue streams may fluctuate unpredictably due to changing customer demand, economic instability, inflationary pressures, or supply chain disruptions. At the same time, expenses such as salaries, rent, and supplier payments often remain fixed or even increase, putting additional pressure on cash flows.

One of the most critical tools for navigating such uncertainty is robust cash flow forecasting. Businesses must develop a detailed and accurate forecast that maps out expected inflows—such as collections from sales—and outflows, including operational expenses, loan repayments, and planned investments.

- An effective cash forecast enables businesses to:

- Anticipate potential shortfalls in advance,

- Align payment obligations with expected income, and

- Assess how well current liquidity and financing facilities cover upcoming expenses.

By proactively identifying cash gaps and planning accordingly, businesses can make informed financial decisions, maintain operational continuity, and mitigate the risk of liquidity crunches—even during turbulent times.

The Role of Cash Flow Forecasting

Businesses must develop a robust cash flow forecasting process to gain clear visibility into their future financial position. This involves accurately projecting both incoming cash flows from sales and collections, and outgoing cashflows related to payments and operational expenses.

- A detailed and reliable cash flow forecast enables companies to:

- Understand their upcoming payment obligations

- Assess the timing and magnitude of cash inflows from customers and other sources

- Identify potential cash shortfalls or surpluses well in advance

- Evaluate how well these obligations are covered by internal cash generation and available financing facilities

By maintaining an accurate cash forecasting system, businesses can make informed decisions, optimize liquidity management, and ensure they have sufficient funds to meet their commitments even during periods of volatility or uncertainty.

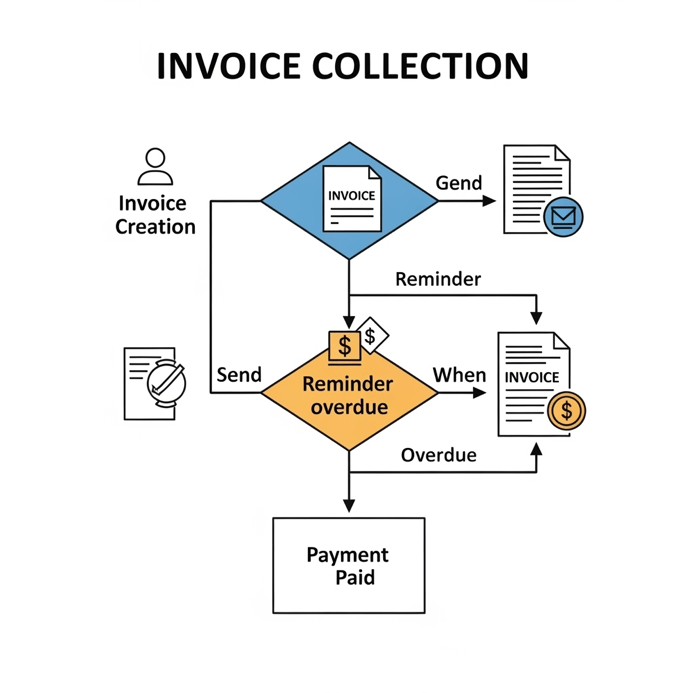

Strengthening the Collection Process

A robust receivables collection process is essential for businesses to maintain healthy liquidity. Timely collection of outstanding sales receivables ensures that cash does not remain unnecessarily tied up, allowing the company to use those funds to meet its payment obligations.

To strengthen the collection process, businesses should:

- Implement a clear and structured framework for managing receivables

- Utilize effective tools and systems to monitor aging invoices and automate reminders

- Align efforts across sales, finance, and customer service teams to enhance collection efficiency

By streamlining collections, companies can reduce the cash conversion cycle, improve cash availability, and better support their operational and financial commitments.

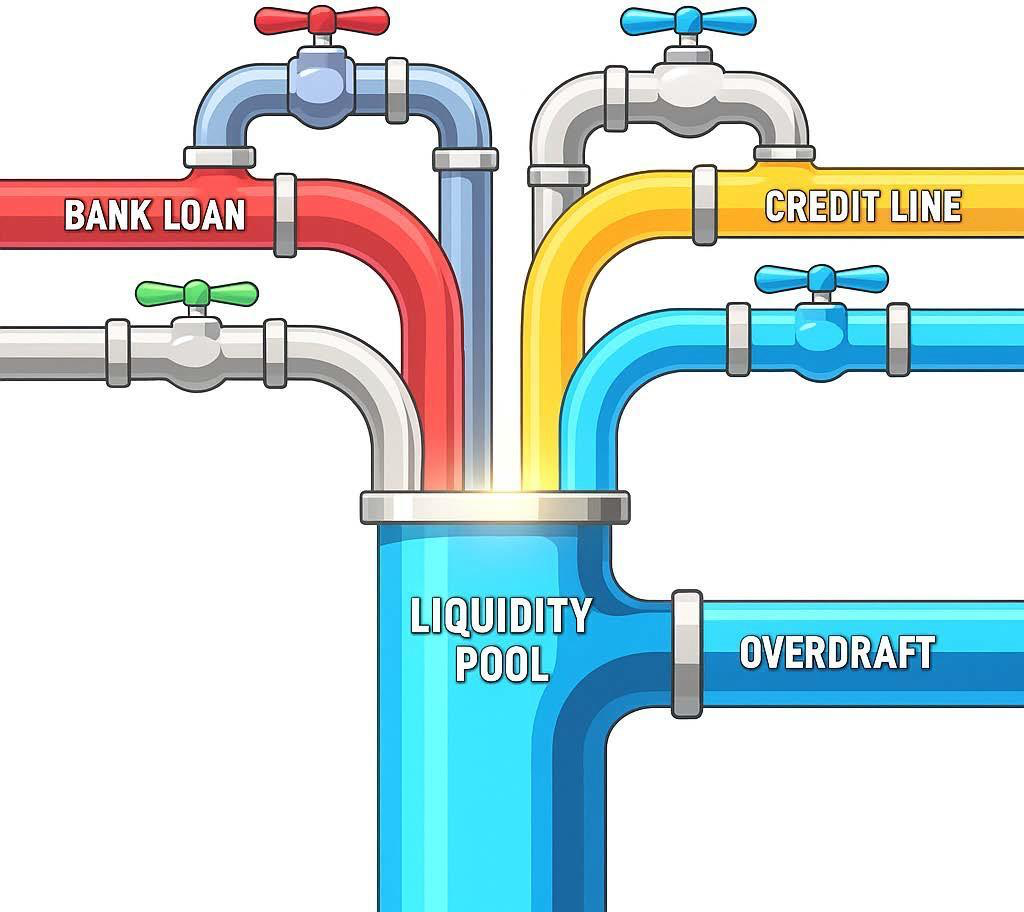

Securing Reliable Financing Facilities

Businesses must ensure access to a range of financing facilities, including both committed and uncommitted credit lines. These facilities serve as crucial liquidity buffers, providing quick access to funds during times of financial stress or unexpected cash flow shortfalls.

Having reliable and sufficient credit facilities in place allows companies to:

- Meet their payment obligations promptly, even in crisis situations

- Maintain operational continuity without disruption

- Enhance financial flexibility to navigate periods of volatility and uncertainty

By proactively securing diverse and dependable financing options, businesses can safeguard themselves against liquidity risks and build resilience for future challenges.

Optimizing the Funding Mix

Companies need to maintain an appropriate funding mix that balances different financing sources to effectively manage liquidity risks. This includes a strategic combination of:

- Short-term and long-term financing options to align with varying cash flow needs and investment horizons

- Fund-based facilities (such as loans and overdrafts) and non-fund-based facilities (such as letters of credit and bank guarantees) to provide flexibility in managing obligations

- Diverse maturity profiles that match payment schedules, ensuring that repayments do not cluster and strain cash flows

- Maintaining a sufficient cash buffer to cover unforeseen expenses or delays in cash inflows, especially during periods of market volatility or economic uncertainty

By carefully optimizing their funding mix, companies can improve financial stability, reduce refinancing risks, and ensure consistent availability of liquidity to support ongoing operations and growth.

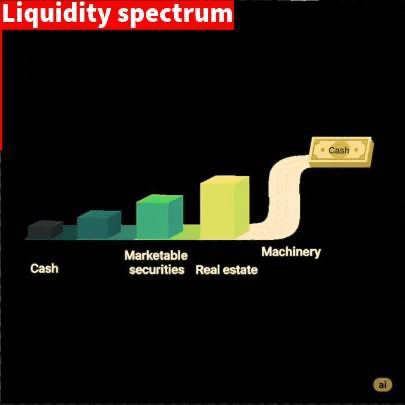

Evaluating Asset Liquidity

It is crucial for businesses to carefully assess the liquidity of their assets, whether held as cash, investments in securities, or other asset classes. The ability to quickly convert assets into cash without significant loss of value is vital, especially during periods of financial stress.

Having a disproportionate share of investments in illiquid assets can create challenges in a liquidity crunch, as these assets may be difficult to sell promptly or may need to be sold at a steep discount. Therefore, maintaining a larger proportion of investments in liquid asset classes is essential, even if it means accepting a slightly lower return.

By prioritizing asset liquidity, companies can ensure they have ready access to funds when needed, enhancing their ability to navigate volatile and uncertain business environments.

Benchmarking Cost of Capital and Banking Fees

Businesses often overlook hidden costs within their financing arrangements. Benchmarking the cost of capital and banking fees ensures that companies are not paying more than necessary for access to funds. It also provides an opportunity to renegotiate terms and improve financial efficiency.

Why Benchmarking Matters:

- Cost of Capital: The weighted average cost of capital (WACC) affects investment decisions and valuation. High capital costs reduce margins and hinder competitiveness.

- Banking Fees: Recurring charges like loan processing, overdraft interest, trade finance fees, and foreign transaction costs can erode profits.

Best Practices:

- Conduct regular comparisons of interest rates, spreads, and fees across banks and markets.

- Use third-party consultants or financial advisors to gather competitive intelligence on fee structures.

- Benchmark against industry peers to identify gaps and optimize negotiation points.

- Track non-obvious fees, such as prepayment penalties or collateral management costs.

Example:

A mid-sized manufacturing firm saved 0.75% in annual interest by switching from a local lender to a multinational bank after benchmarking revealed above-average charges.

Explore Alternative Legal Entity Structures to Optimize Tax

Corporate structure directly impacts tax efficiency, regulatory exposure, and liquidity movement. Businesses operating in multiple jurisdictions can benefit from legal structuring to reduce tax burden, optimize funding flows, and support future expansion.Corporate structure directly impacts tax efficiency, regulatory exposure, and liquidity movement. Businesses operating in multiple jurisdictions can benefit from legal structuring to reduce tax burden, optimize funding flows, and support future expansion.

- HoldCo/SubCo Structures: Establishing holding companies in tax-efficient regions (e.g., Netherlands, Ireland, Singapore) for managing dividends, IP, and royalties.

- IP Box Regimes: Centralizing intellectual property in jurisdictions with favourable tax rates on IP income.

- Intra-group Service Entities: Creating shared service centres to streamline cross-border operations and allocate costs tax-efficiently.

Key Considerations:

- Compliance with OECD BEPS (Base Erosion and Profit Shifting) standards.

- Ensuring sufficient economic substance in entities to avoid regulatory scrutiny.

- Understanding transfer pricing rules and how profits are allocated between countries.

Trapped Cash Repatriation

Trapped cash refers to earnings held by foreign subsidiaries that cannot be freely transferred to the parent company due to tax penalties, local laws, or regulatory capital requirements.

Common Trapping Scenarios:

- Currency controls or dividend withholding taxes.

- Local banking restrictions or minority shareholder constraints.

- Capital adequacy requirements in regulated industries (e.g., insurance, banking).

Techniques to Unlock Trapped Cash:

- Intercompany Loans: Lending cash from foreign units to the parent or other subsidiaries.

- Management Fees/Royalties: Charging subsidiaries for group-level support services.

- Capital Reduction/Buyback: Reducing equity in subsidiaries to release funds.

Case Insight:

A global software company repatriated $50M from its Asian operations by restructuring intercompany pricing and using management fee arrangements compliant with local laws.

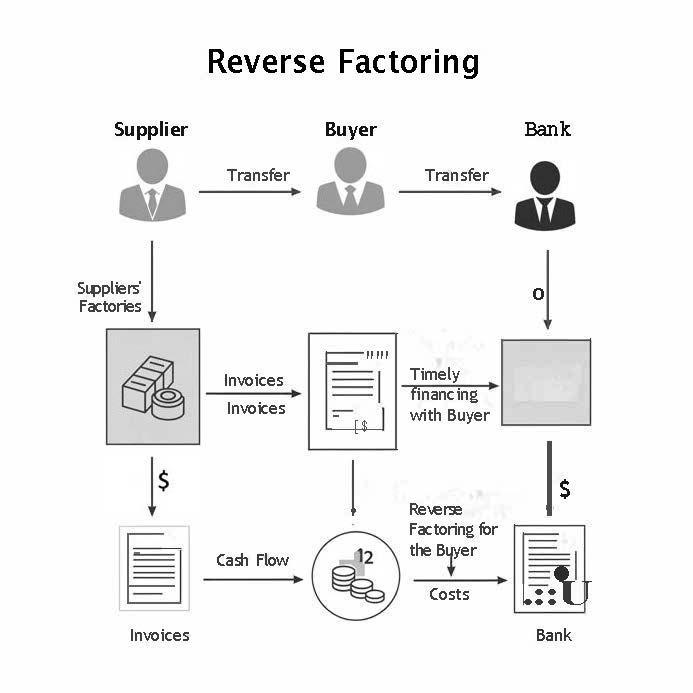

Alternative Supply Chain Financing Strategies

Supply chain financing (SCF) enables companies to strengthen liquidity while supporting suppliers. Especially during market disruptions, these tools improve working capital without affecting operations.

Key SCF Options:

- Reverse Factoring: Buyers initiate early payments to suppliers, financed by a bank, improving supplier cash flow while buyers retain longer payment terms.

- Dynamic Discounting: Buyers use excess liquidity to pay suppliers early in exchange for discounts.

- Inventory Financing: Lenders provide credit using unsold inventory as collateral, freeing up capital stuck in stock.

Benefits:

- Preserves supplier relationships.

- Reduces cost of capital for suppliers, especially small vendors.

- Protects operational continuity during credit shortages.

Asset-Heavy vs. Asset-Light Capital Models

Capital model selection has deep implications for liquidity, risk, and strategic flexibility. Understanding the trade-offs helps tailor the model to business needs.

Asset-Heavy Model:

- Owns infrastructure: Factories, warehouses, fleets.

- Pros: Long-term cost control, collateral for loans, full operational control.

- Cons: High upfront investment, low agility in downturns.

Asset-Light Model:

- Leases or outsources assets: Focus on IP, branding, or distribution.

- Pros: Low capital intensity, scalable, faster cash returns.

- Cons: Higher recurring expenses, potential vendor risk.

Decision Factors:

- Industry lifecycle (growth vs. maturity),

- Cash flow predictability,

- Volatility in demand.

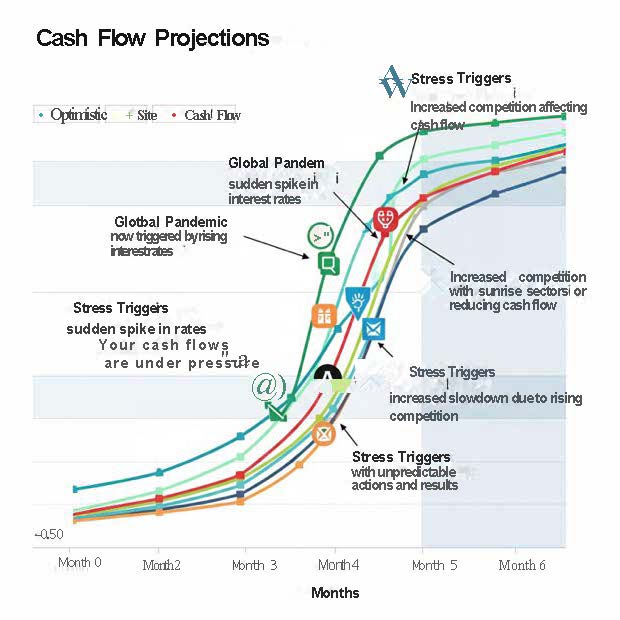

Scenario Analysis for Market Risk Management and Business Continuity Planning

Volatile markets demand that businesses test their financial resilience using multiple scenarios. This approach allows organizations to model outcomes and prepare responses in advance.

Key Elements:

- Scenario Types:

- Base Case: Normal business expectations.

- Downside: Market crash, sales drop, currency devaluation.

- Stress Case: Simultaneous adverse events (e.g., demand drop + cost hike + FX loss).

- Financial Variables Modeled:

- Cash flow, interest rates, input costs, FX rates, sales volumes.

- Output:

- Required liquidity buffer.

- Early warning thresholds.

- Crisis response plans.

Sustainability Planning and Initiatives (ESG)

ESG (Environmental, Social, and Governance) factors are increasingly influencing investor decisions and funding access. Integrating ESG into liquidity planning ensures long-term value creation and cost savings.

ESG Initiatives Supporting Liquidity:

- Green Financing Instruments:

- ESG-linked loans with margin discounts for meeting sustainability KPIs.

- Green bonds for clean energy or sustainable supply chain investments.

- Cost Savings:

- Energy efficiency initiatives reducing OPEX.

- Waste management minimizing disposal costs.

- Investor Relations:

- Enhanced access to ESG-focused funds and institutional investors.

- Improved ratings and brand value.

Sale Of Assets and business spin-off

When facing liquidity pressure, businesses may turn to non-core asset sales or spinning off divisions to raise capital and sharpen focus.

Use Cases:

- Divesting underperforming or non-essential divisions.

- Selling real estate, equipment, or IP for cash inflow.

- Creating independent spin-offs with external funding or listing.

Advantages:

- Strengthens balance sheet by reducing debt or boosting liquidity.

- Enhances strategic clarity and operational focus.

- Improves investor perception and valuation.

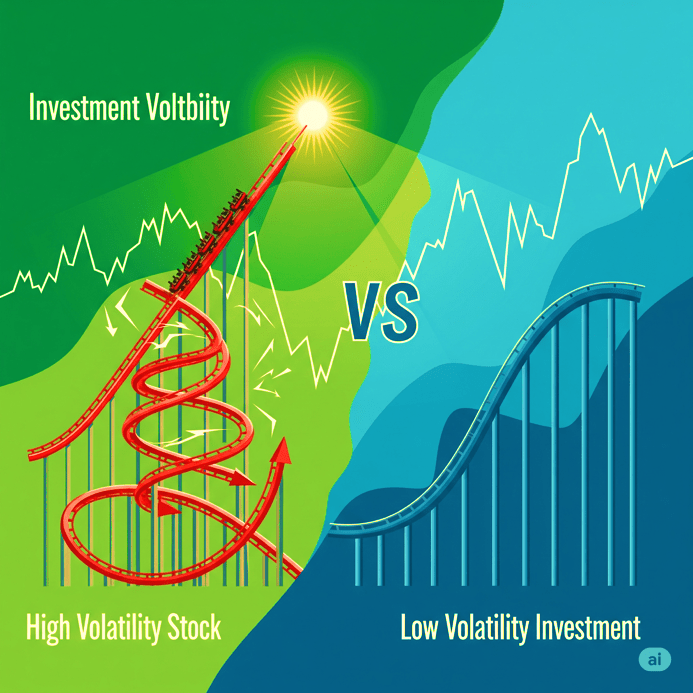

Managing Investment Volatility and Market Risk

It is important for companies to carefully assess the volatility and market risk associated with their investments across different asset classes. Investments in highly volatile assets can pose significant challenges, especially if the company needs to liquidate these investments before their maturity.

Exiting such volatile asset classes prematurely may result in substantial losses, which can negatively impact liquidity and overall financial stability. Therefore, companies should aim to manage their investment portfolio by balancing risk and return, prioritizing assets that can be liquidated with minimal principal loss when needed.

By actively monitoring market risks and adjusting investment strategies accordingly, businesses can safeguard their liquidity and maintain financial resilience in uncertain environments.

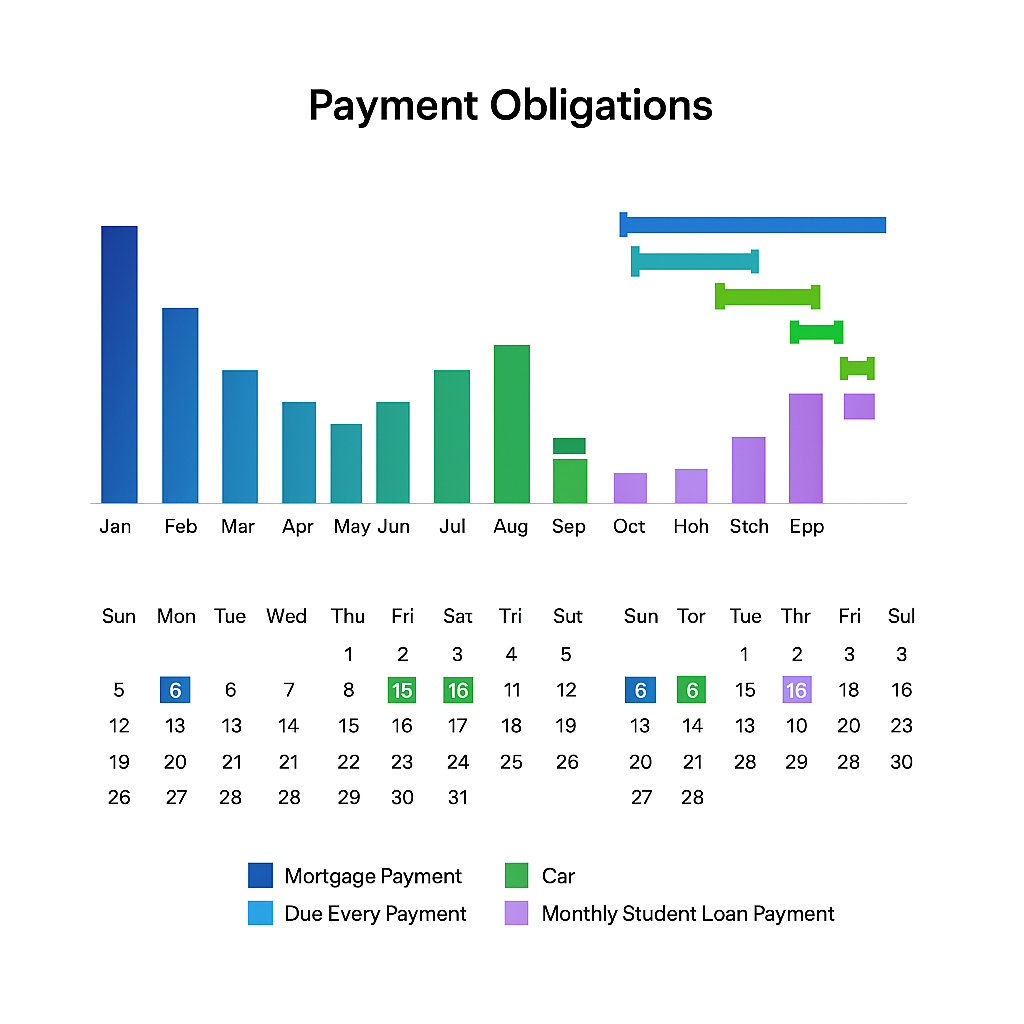

Monitoring Payment Obligations Across Timeframes

Companies need to establish a clear framework and reporting system for tracking their payment obligations across multiple time horizons. This proactive approach ensures that they remain fully aware of upcoming maturities in the short term, medium term, and long term.

By regularly monitoring these obligations, businesses can:

- Anticipate cash outflows and plan accordingly

- Prevent liquidity shortfalls by aligning payments with expected cash inflows

- Make informed financing decisions well in advance of payment deadlines

- Enhance transparency and accountability within the finance team and across management

Implementing such a framework helps organizations maintain better control over their liquidity and reduces the risk of unexpected payment crises, even in volatile and uncertain business environments.

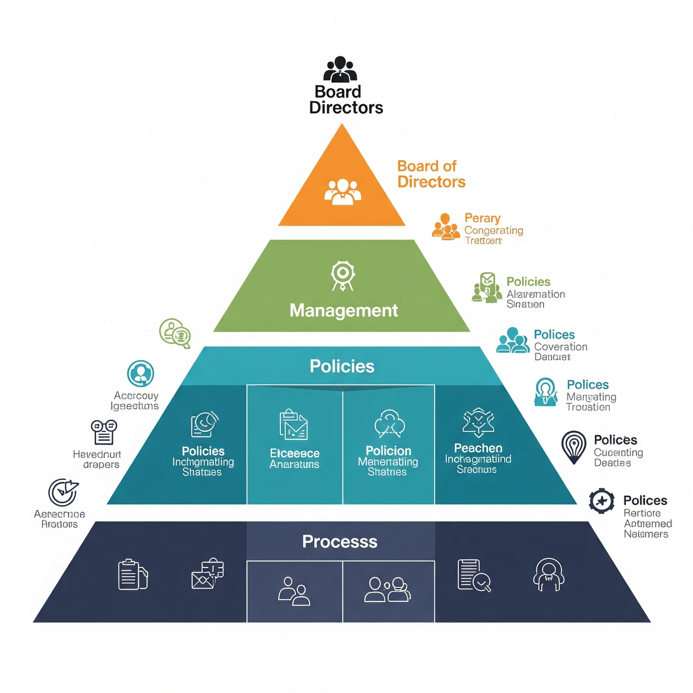

Establishing Liquidity Risk Governance

To sustainably manage liquidity, businesses must implement a comprehensive governance framework for liquidity risk management. This includes well-defined policies, processes, and oversight mechanisms that guide how liquidity risks are identified, measured, monitored, and mitigated.

Key components of effective liquidity risk governance include:

Such a governance structure enables businesses to scale operations confidently while minimizing the risk of liquidity constraints that could hinder growth or lead to financial distress.

Implementing Continuous Review and Performance Monitoring

An effective liquidity management strategy requires an ongoing process of continuous review and performance monitoring. Businesses must regularly assess their financing facilities, investment portfolios, and overall liquidity position to identify emerging risks and opportunities for improvement.

Key practices include:

- Periodic evaluation of financing arrangements to ensure terms remain competitive and aligned with evolving business needs

- Monitoring the performance and liquidity of investments to detect shifts in market conditions or asset quality

- Tracking compliance with internal liquidity policies and limits

- Establishing feedback loops for timely corrective actions when deviations or risks are detected

- Utilizing dashboards and reporting tools to provide real-time insights to management

- By embedding continuous review into their liquidity management processes, companies can proactively mitigate liquidity risks, adapt swiftly to changing market environments, and sustain operational stability.

Conclusion:

In today’s volatile and uncertain business landscape, managing liquidity is not merely a financial best practice—it is a strategic imperative. From accurate cash flow forecasting to disciplined collection processes, diversified financing, and robust governance, every aspect of liquidity management must be proactively and continuously refined.

Organizations that embrace an integrated, forward-looking approach to liquidity can better weather economic shocks, respond agilely to market disruptions, and sustain long-term growth. By institutionalizing sound liquidity practices and fostering a culture of financial discipline, companies not only secure their present operations but also build a resilient foundation for future success.

Ultimately, effective liquidity management transforms uncertainty from a threat into an opportunity—empowering businesses to thrive, not just survive.

Our flagship treasury consultation program – “Managing liquidity in a volatile and uncertain business environment” assists you to enhance the robustness of your financial risk management process. Please get in touch with us at info@hedgeitright.com to know more.

business innovation cash flow cash forecast cost control entrepreneurship financial discipline financial planning financial risk forecasting internal funding Liquidity risk organic growth risk management startup strategy sustainable business value creation

Leave a comment